The Best 529 Plans

Taking advantage of tax benefits by investing in low-cost, smartly designed 529 plans can stretch your college savings dollars.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

Editor’s note: We have published new research and enhanced our methodology. Read our evaluation of the top 529 college savings plan of 2020.

There are lots of benefits to using 529s to save for future college costs. They are funded with aftertax dollars, which then grow tax-free. Withdrawals for qualified education expenses are also tax-free. On top of that, some states offer tax deductions or credits for contributions.

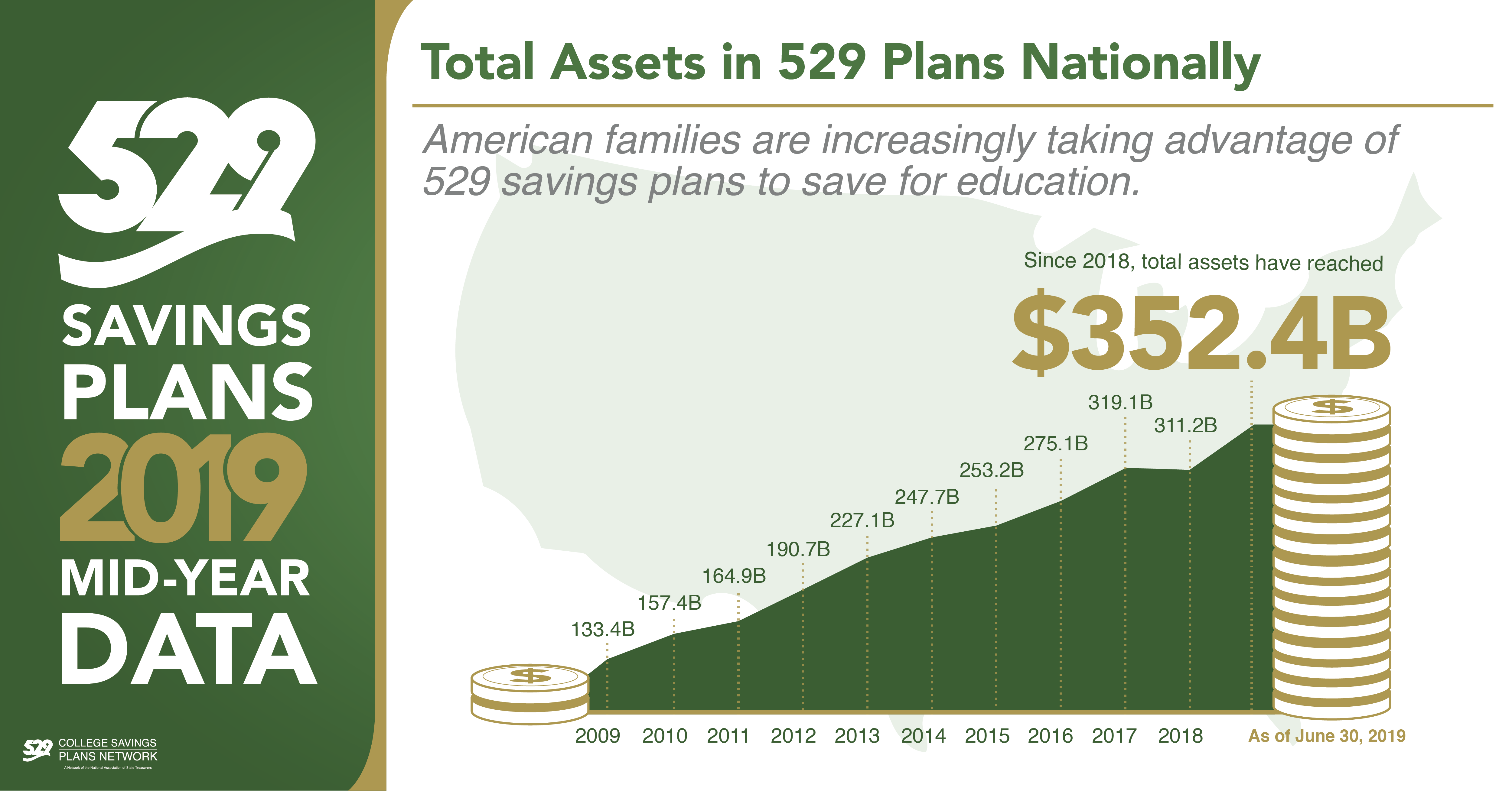

Because of these money-saving tax benefits, 529s are becoming increasingly popular: According to data from the College Savings Plan Network, U.S. families had invested more than $350 billion in 529 accounts as of June 30, 2019.

But not all 529 plans are created equal. Some plans are saddled by high fees and poor investment choices, which can hamper your savings progress and erode your returns. Morningstar analysts carefully evaluate 529 plans and assign Morningstar Medalist ratings based on their scores in five key areas: Process, People, Parent, Price, and Performance.

If your state's plan leaves much to be desired, you have no obligation to invest in it. Investors are free to choose nearly any state's plan. If you live in a state that doesn't offer any tax benefits for 529 contributions, or a state that offers tax benefits regardless of which state's 529 plan you use (these are commonly referred to as tax-parity states), you may want to take a look at the plans Morningstar analysts have awarded Gold, Silver, or Bronze medals.

If you live in a state that does offer tax benefits for using the in-state plan, though, they should factor into your decision-making.

The four plans profiled below earn Morningstar Analyst Ratings of Gold. Premium members can read in-depth analyses of all plans under coverage in the 529 Plan Center on Morningstar.com.

The Illinois Bright Start Direct-Sold College Savings Program boasts an impressive fund lineup, strong plan oversight, and competitive fees. It remains a top choice for college savers.

This plan has two types of aged-based offerings: a multi-firm one that invests primarily in actively managed funds, and an index one that uses low-cost Vanguard funds. Both options offer three tracks: aggressive, moderate, and conservative, starting with 100%, 90%, and 80% equity allocation, respectively. Each track includes nine steps, which makes it relatively smooth; smoother glide paths have been shown to lead to less-volatile returns for investors while offering some minor downside protection.

Illinois residents also enjoy further benefits--contributions up to $10,000 can be deducted when calculating state income taxes. --Patricia Oey

With diligent state oversight, strong underlying funds, and a more institutional-level approach to asset allocation, Virginia's Invest529 plan is a cut above.

The age-based portfolios contain a good balance of low-cost index funds and active funds that have the potential for outperformance. The plan's affordability remains a benefit, though it has lost some ground to peers as fees fall across the industry. The plan also offers a number of cheap stand-alone portfolios for investors looking to be more hands-on with their investments.

Virginia residents may deduct up to $4,000 of contributions from their state income, leaving little reason to look elsewhere. Nonresidents may also want to size it up against other plans. --Bobby Blue

This top-rated 529 plan seeks to provide a high level of investor choice. It was the first plan to offer customized age-based options, allowing investors to design a glide path from scratch and select from a broad suite of funds to build each portfolio. The underlying funds available in the custom investment options, as well as additional stand-alone choices, are a mix of proven strategies. There is a suite of Vanguard funds, all 19 of which carry Morningstar Medalist ratings, and 10 DFA strategies, seven of which are Morningstar Medalists.

The plan also offers four preset age-based tracks. Two of the tracks--Aggressive Domestic and Aggressive Global--follow the same asset-allocation glide path, with the former only holding U.S. equities and the latter holding both U.S. and non-U.S. stocks. The Moderate and Conservative tracks provide global exposure to stocks and invest primarily in low-cost, broad-based Vanguard index funds.

Utah residents can claim a state income tax credit of up to $200 for contributions. -- Madeline Hume

This 529 stands out for its low costs and demonstrated commitment to industry best practices. Participants can choose between two age-based portfolio tracks, one active and one passive. They are both among the lowest-cost versus similar direct-sold options, and going forward the portfolios will use a more gradual path to reduce their equity exposure over time.

The active age-based track's underlying funds, which consist of best-in-class managers regardless of fund company affiliation, are another bright spot. Some of the highly regarded fixed-income funds include Gold-rated Metropolitan West Total Return and Silver-rated PIMCO Income. On the equity side, most assets are managed by T. Rowe Price and DFA, two well-regarded equity managers.

The state of California does not offer a tax benefit for 529 plan contributions. --Jason Kephart

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

{kind=link}